Term Insurance vs. Life Insurance (2026): Separating protection from investment is the key to financial freedom.

For most Indian families, Term Insurance is the clear winner for life protection in 2026—offering massive coverage at a fraction of the cost.

Traditional Life Insurance suits only conservative savers who prioritize guaranteed maturity and can accept significantly lower life cover.

Whenever it comes to choosing the right life insurance for us, we ask the agents this question. “Kitna Dene Se Kitna Milega?” It means if I pay sum X, then how much will I get in future? Isn’t it? Can you relate yourself to this question?

For many of us, the answer would be a BIG yes! We completely ignore the protection part while giving value to the investments only. Choosing the right insurance product is crucial for you and your family. In this detailed guide, we will settle the debate of Term Insurance vs. Life Insurance once and for all.

Executive Summary: Term vs. Life Insurance Verdict (2026)

Don’t lose this data. Download the high-resolution 2026 comparison chart or share it with your family to help them make the right choice.

From the ages in India, most people treat insurance as an investment. This is due to our financial illiteracy. Still, schools in India do not have any specific subject/course in personal finance.

Our parents and insurance agents have taught us for decades a valuable lesson. They say, “If we pay a premium, we must get some money back”. As a result, every time we end up buying “high premium, low sum assured, worthless ” life insurance policies.

The debate between Term Insurance and Traditional Life Insurance, especially traditional endowment or whole life plans, is intensifying as we approach 2026. Rising medical costs and changing tax laws mean buying insurance is now a strategic financial decision.

We will explain why separating your insurance from your investment is crucial. It is the golden rule of personal finance. We will help you decide which policy is best suited for you.

In the evolving financial environment of 2026, there is an essential difference between term insurance and traditional life insurance. This difference involves more than just death benefits.

It extends far beyond mere death benefits. It’s fundamentally about optimising the use of your capital and achieving the best possible financial outcomes.

This means prioritising the most effective strategies for protection and wealth creation. It is more important than simply focusing on the potential returns or benefits linked to a policy. This is especially true for traditional life insurance policies.

Term Insurance is the simplest and most affordable form of life assurance. It is a pure protection plan. Think of it like “renting” safety for your life. As long as you pay the rent (premium), your family is protected even at a lower cost. Its main focus is affordable pure life protection and nothing else, unlike traditional life insurance.

It is strictly for sole breadwinners. If your family relies on your income to meet daily needs, you need Term Insurance immediately. It is also necessary if they depend on you to pay for rent, school fees, or loans. However, you may also opt for the Married Women’s Property Act, 1874, for extended security of the death benefits.

Under the Married Women’s Property Act, the husband can obtain a policy for his wife and children. In such cases, the death benefits are solely owned by the wife. The policy guarantees that the benefits are exclusively hers. They are protected from any legal seizure by a court of law.

When people say “Life Insurance” in India, they usually mean Endowment Plans, Money Back Policies, or Whole Life Plans, popularly known as the traditional life insurance policies. This is the most trusted and sought-after life insurance policy in India.

These are sold as “Savings Plans, Money Back guarantee, Capital Protection.” But forgot to deliver adequate death coverage to the insured person. This is the harsh reality of traditional life insurance policies in India.

To obtain a ₹1 Crore life cover with a traditional endowment plan, you might need to pay a high annual premium. This premium could be around ₹5 Lakhs to ₹10 Lakhs. Due to the high premium costs, many individuals choose policies with inadequate coverage.

For example, they might select a policy with a sum assured of ₹5 Lakhs. This amount is often insufficient to meet their family’s future financial needs. This makes the policyholder an under-insured person.

Presently, the majority of the Indians are standing upon this under-coverage insurance.

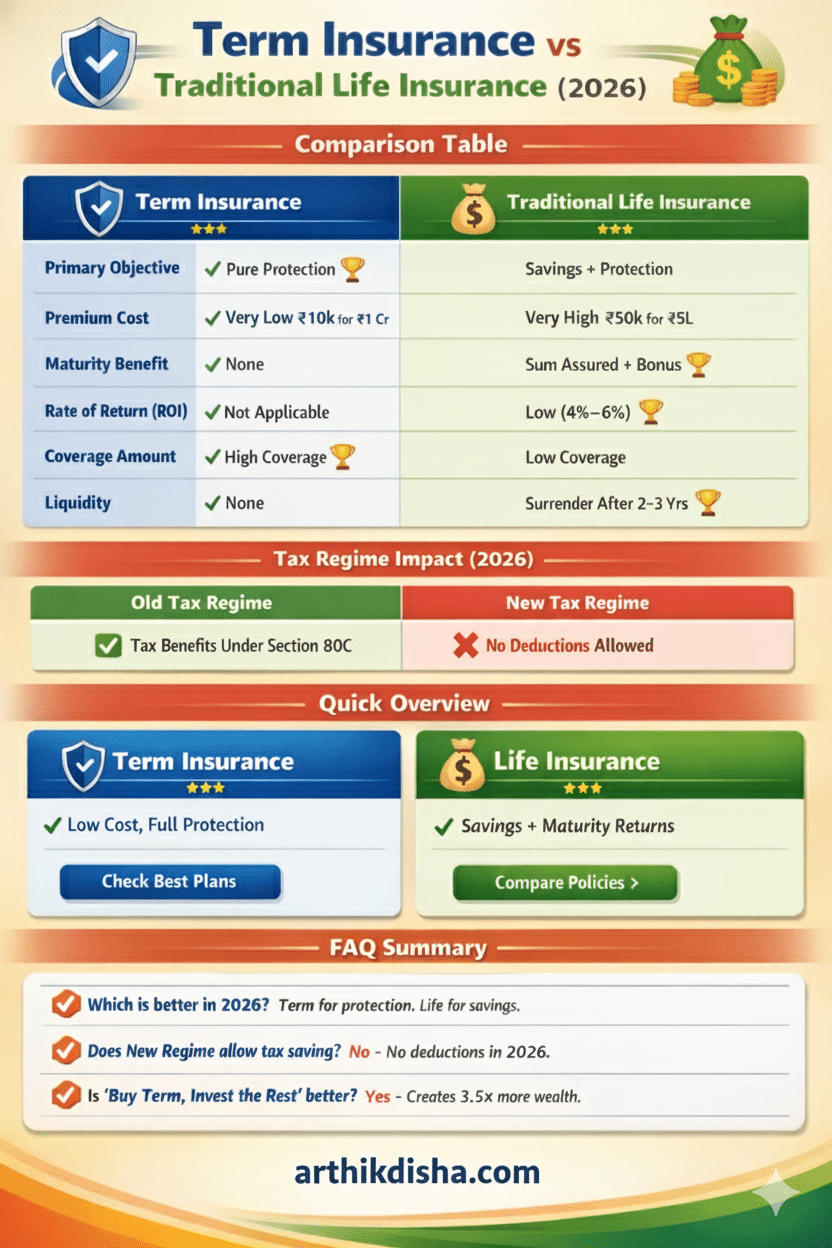

| Feature | Term Insurance | Traditional Life Insurance |

|---|---|---|

| Primary Objective | Pure Financial Protection 🏆 | Investment + Protection |

| Premium Cost | Very Low (₹10k for ₹1 Cr) 🏆 | Very High (₹50k for ₹5L) |

| Maturity Benefit | None (Expense) | Sum Assured + Bonus 🏆 |

| Rate of Return (ROI) | Only on Death | Low (4%–6%) |

| Coverage Amount | High (Income Replacement) 🏆 | Low Coverage |

| Tax Benefit (80C) | Yes-Old Regime* | Yes Old Regime* |

| Liquidity | None | Low (After 2–3 yrs) 🏆 |

This is the ideal financial strategy. Every school should teach their students about it. They should take advantage of such valuable lessons once they start earning. This helps them avoid falling prey to buying high-premium endowment plans.

The main goal is to secure affordable life insurance coverage (Buy Term) through term insurance while investing the remaining ( Invest rest ) amount in mutual funds for the duration of the policy. This strategy is often advised by the SEBI-registered Investment Advisers.

Let’s look at the math with a real-world example.

Scenario: Gopal Krishnan (Age 30) wants to invest ₹50,000 per year for 20 years. He has two choices:

Option A: Traditional Endowment Plan

Option B: Term Insurance + Mutual Funds (The Smart Way)

🏆 The Verdict: Why Option B (Term + Mutual Funds) Wins

In our analysis of Krishnan’s financial profile, Option B is the clear winner for three critical reasons:

Final Conclusion: For 2026, separating insurance from investment is the most mathematically sound strategy for Indian families. People still fall prey to insurance mis-selling due to a high incentive structure for the agents.

Both types of insurance are tax-efficient, which is why they are popular in March every year(tax season).

Choosing the best term insurance plan in India for 2026 is no longer just about low premiums. With rising awareness, policyholders now focus on claim settlement ratios, solvency ratios, insurer reliability, long-term stability, and rider benefits. Here are the top picks by ArthikDisha:

As per the IRDAI Annual Report 2025 (latest available data), three insurers consistently stand out in India’s term insurance space:

Below is a data-driven analysis. It explains why these insurers are considered among the best term insurance plans in India for 2026.

LIC maintains its position as the most trusted life insurer in India. Salaried individuals particularly trust it. Families who are planning for long-term financial security also trust LIC.

As per the latest IRDAI report, LIC demonstrates consistent claim settlement, thereby reinforcing its position as a reliable insurer.

📌 Best for: Risk-averse individuals, government employees, long-term planners

📌 Popular plan: LIC Tech Term / LIC New Jeevan Amar

HDFC Life Insurance is recognised for its robust claim performance. It is also committed to digital convenience. This establishes it as a preferred option for tech-savvy and urban policyholders.

IRDAI data shows HDFC Life consistently ranks among the top private insurers for claim settlement and customer grievance resolution.

📌 Best for: Salaried professionals, digital-first buyers

📌 Popular plan: HDFC Life Click 2 Protect Super

ICICI Prudential Life Insurance offers a comprehensive approach, integrating affordability, strong claim settlement rates, and flexible coverage options, positioning it as a suitable selection for families and young professionals.

IRDAI’s insurer performance data places ICICI Prudential among the most consistent private life insurers in India over multiple years.

📌 Best for: Young earners, families, long-term protection seekers

📌 Popular plan: ICICI Pru iProtect Smart

IRDAI publishes annual performance data, including:

Utilising the IRDAI Annual Report 2025, which is the most recent data available, is beneficial. This ensures your term insurance decisions for 2026 planning are based on verified industry data. This approach relies on verified industry data rather than marketing assertions.

As I already discussed that the primary notion is like Kitna Dene Se Kitna Milega. People often see insurance as an investment. It is quite hard for them to believe that insurance should be perceived as the ” pure protection plan “.

However, when considering the comparison between term life insurance vs life insurance, individuals should prioritise pure life protection and opt for affordable, straightforward term insurance with comprehensive coverage.

Let’s look at Rahul (30 years old, Non-smoker) who wants a ₹1 Crore cover for 30 years.

| Plan Type | Annual Premium (Approx) | Benefit if he dies at 45 | Benefit if he survives to 60 |

| Term Insurance | ₹12,000 | ₹1 Crore | ₹0 |

| Endowment Life Plan | ₹1,50,000 | ₹1 Crore + Bonus | ₹50 Lakh (Guaranteed + Bonus) |

Result: By choosing Term Insurance, Rahul saves ₹1,38,000 per year, which he can use to fund his child’s education or retirement through SIPs.

In 2026, financial literacy is about making every rupee count. While traditional Life Insurance policies offer the comfort of “getting something back,” they often fall short on their primary purpose: pure protection. This leaves you underinsured and with returns that barely outpace inflation.

Our Recommendation:

Know the difference between investment vs insurance. Keep them separate, and your financial future will be fully secure in case of any unprecedented incident.

Married Women's Property Act India or MWP Act 1874 was enacted in the year 1874…

Official Advisory AY 2027-28 Updates Quick Highlights: Download Form 16 Toolkit ✔ Updated Form 16…

A disciplined 4-step framework to select the best term insurance plan in India, based on…

2026 BUDGET UPDATE Immediate Action: For FY 2026-27, the New Tax Regime is your default…

Download the official ArthikDisha Income Tax Calculator for FY 2026-27. Compare Old vs New regimes…

OFFICIAL ADVISORY 2026 Immediate Action: For 2026, we recommend keeping your annual cash deposits below…

{kind=link}