2026 Official Advisory: Beat 14% Inflation with the 3-Year Rule.

Immediate Action: With medical inflation hitting 14% in India, a ₹5 Lakh cover is no longer a safety net—it is a risk. For 2026, we recommend a baseline of ₹25 Lakhs for Metro families. Prioritize plans with “Unlimited Restoration” and “No Room Rent Caps” to avoid massive out-of-pocket hospital bills.

Imagine waking up to a hospital bill that is 14% higher than it was just twelve months ago. For the majority of Indian families, this is not hypothetical. It is the current reality of medical inflation in India, as projected for 2026. Rising healthcare costs, for both routine care and emergencies, are rapidly outpacing the savings of many of us.

As the primary breadwinner, ensuring comprehensive family care without financial strain is key. This Health Insurance Guide 2026 for Families analyses the practical implications of the 2026 IRDAI regulations, empowering informed decision-making.

With the introduction of the 3-year rule for pre-existing conditions and new moratorium regulations, 2026 marks a shift in insurance, favouring the common man. This guide will help navigate the 2026 health insurance landscape, securing the best family coverage in India without overspending.

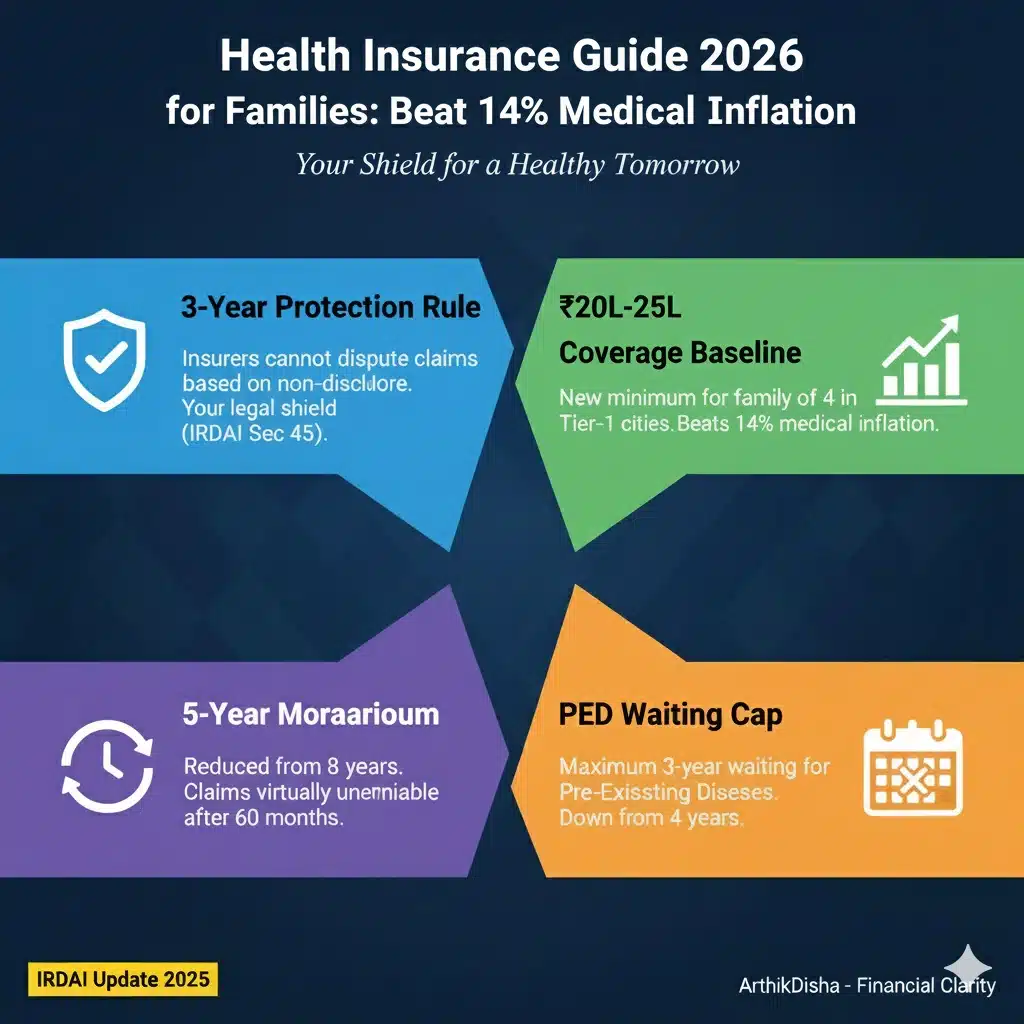

Under IRDAI’s Section 45, once your policy (Life or Health) is 3 years old, insurers cannot dispute claims based on non-disclosure. This is your primary legal shield.

For a family of four in a Tier-1 city, ₹20L to ₹25L is the new minimum. Anything less fails to cover the 14% annual surge in medical inflation.

The moratorium period is now reduced from 8 years to 5 years. After 60 months of continuous renewal, your claims become virtually undeniable by the insurer.

Mandatory waiting periods for Pre-Existing Diseases (PED) are now capped at a maximum of 3 years, down from the previous 4-year limit.

Don’t miss this important insight. Download the high-resolution 2026 Health Insurance Guide or share it with your family to help them stay protected from rising medical inflation.

Health Insurance in 2026: How Indian Families Can Beat 14% Medical Inflation: India’s medical inflation is projected to hover around 14% in 2026, making healthcare one of the fastest-rising household expenses.

For Indian families, a single hospitalisation could deplete years of savings if their health insurance is inadequate or outdated due to the surge in medical costs.

Health insurance in 2026 requires more than just a policy; it demands the right sum insured, appropriate room rent limits, broader disease coverage, and inflation-adjusted benefits. Many families continue relying on outdated policies, unaware that rising treatment costs have silently diminished their actual protection.

If you feel like your health insurance premium is increasing faster than your salary, you aren’t imagining it. According to the 2026 Global Medical Trend Rates Report, India is witnessing a “medical trend” of 11.5% to 14%.

To put that in perspective, while general inflation (CPI) might hover around 4%, the cost of a hospital bed or a cardiac stent is rising nearly three times faster.

The ArthikDisha Insight: “Medical Inflation” isn’t just about the bill you pay, it’s about the ‘Sum Insured’ you hold. If you bought a ₹5 Lakh policy in 2021, its actual purchasing power in 2026 is closer to ₹3 Lakh. You aren’t just paying more, you’re actually getting less protection unless you upgrade.

The most significant update is the reduction of the Pre-existing Disease (PED) waiting period. IRDAI has taken a really good step by taking into consideration the “customer first approach“.

As per Section 45 of the Insurance Act, 1938, the IRDAI has issued a Master Circular on 29 May 2024, under the “Insurance for all by 2047″ policy, whereby no health insurance policy can be contested after 36 months of continuous coverage.

This “Health Insurance 3 Year Rule” ensures that your policy becomes “Claim Secure”. It is effective after 3 years of continuous policy premium payment. It’s a massive financial shield for families dealing with chronic health conditions.

Beat the 14% inflation gap with monthly expert updates.

🔒 Join 5,300+ informed Indian families.

Have you ever worried that an insurance company might dig up a 10-year-old medical record to reject your claim today? Under the new mandates, the moratorium period in health insurance has been reduced from 8 years to 5 years.

What this means for you: If you have renewed your policy continuously for 5 years, the insurance company cannot reject your claim due to non-disclosure. They also cannot reject it for misrepresentation unless they can prove deliberate fraud.

It’s like a “statute of limitations.” It guarantees your claim’s safety. This is valid once you’ve been a loyal customer for five consecutive years. This is a great move by IRDAI, undoubtedly.

To make the most of these rules, here is a quick checklist:

In 2026, rising medical inflation in India (estimated 12–14% annually) has made family health insurance no longer optional—it is essential. A well-chosen family floater health insurance plan can protect your savings.

It offers cashless treatment across thousands of hospitals. Additionally, it provides tax benefits under Section 80D under the Old Tax Regime.

The term ” how much ” actually is not the same for all. It depends on various factors. These include the number of your family members, your city of residence, and your income level. Check the table below for a better understanding:

| Family Composition | Location (City Type) | Recommended Cover (2026) |

|---|---|---|

| Young Couple (Below 40) | Tier 2 / Tier 3 | ₹10 Lakh – ₹15 Lakh |

| Nuclear Family (2+2) | Metro / Tier 1 | ₹20 Lakh – ₹25 Lakh |

| Joint Family (5+ Members) | Metro Cities | ₹30 Lakh – ₹50 Lakh |

| Family with Senior Citizens | Any City | ₹25 Lakh + ₹50L Super Top-Up |

To be very honest, early entry in the insurance market is essential. This helps to beat the rising insurance premiums. The bottom line is that “ the earlier you take an entry, the lower the premium” will be for you.

One may find it a waste of money during the earlier periods. However, it will definitely become handy as you grow older. The inclusion of IRDAI’s new rules, such as the 3-year rule and the 5-year moratorium rule, will be beneficial.

Choosing a health plan in 2026 isn’t solely about the lowest price. It’s also about preventing the 14% medical cost surge. This can lead to large bills despite having insurance. One should look for a ” protection first and premium later ” approach. Many families overlook coverage in favour of premiums.

To help you “future-proof” your finances, I’ve broken down the most reliable plan structures for 2026. Whether you are a young professional in a Tier-2 city or managing a multi-generational household in a Metro, the table below reveals the estimated annual costs and the ideal “Sum Insured” you should aim for.

ArthikDisha Pro-Tip: If you live in a Metro city, don’t settle for less than ₹20 Lakh. Between rising room rents and advanced surgical costs, a smaller cover might vanish in just one major hospitalization.

With the new IRDAI 3-year rule, switching policies is easier, but keeping your original start date is vital for the 5-year moratorium benefit.

| Plan Type | Base Cover | Annual Premium (Est.) | Ideal For |

|---|---|---|---|

| Basic Family Floater | ₹10 Lakh | ₹13,500 – ₹20,000 | Young families |

| Comprehensive Plan | ₹20 Lakh | ₹22,800 – ₹34,000 | Metro residents |

| Floater + Super Top-Up | ₹10L + ₹40L | ₹20,500 – ₹28,500 | Cost-conscious buyers |

| Sum Insured | Family of 4 | Family of 5 |

|---|---|---|

| ₹10 Lakh | ₹18,000 – ₹22,000 | ₹22,000 – ₹26,000 |

| ₹20 Lakh | ₹25,000 – ₹30,000 | ₹30,000 – ₹36,000 |

| ₹25 Lakh | ₹30,000 – ₹35,000 | ₹36,000 – ₹42,000 |

Imagine you are eligible for a room at ₹5,000/day, but you choose a private room at ₹8,000/day. You might think you’ll just pay the ₹3,000 difference.

However, hospitals in India often “tier” their pricing. In a higher-category room, the rent is higher. The Surgeon’s fee, Anesthesia charges, and Nursing costs also increase proportionately. If you exceed your room rent limit, the insurer will apply a Proportionate Deduction to your whole claim.

The “ArthikDisha” Example:

2026 Strategy: Always opt for a policy with “No Room Rent Capping” or at least “Single Private A/C Room” eligibility. This ensures that a simple choice for privacy doesn’t bankrupt your claim.

Choosing the right plan in 2026 requires looking at “Consumables Cover.” Items like masks and gloves now make up 10-15% of hospital bills. Plans like HDFC Ergo Optima Secure and Niva Bupa ReAssure 2.0 now include this as a built-in feature.

| Feature | Tata AIG | HDFC Ergo | Niva Bupa |

|---|---|---|---|

| Premium (Age 35) | ₹18,500* | ₹21,200* | ₹19,800* |

| Waiting Period | 24 Months | 36 Months | 36 Months |

| Restoration | Once | Unlimited | Unlimited |

| Consumables | Add-on | Built-in | Built-in |

| 2026 Verdict | Best for Chronic Illness (Short Wait) | Best for Max Coverage (2X/3X Boost) | Best for Long-Term Value (Age Lock) |

ArthikDisha Pro-Tip: While deciding the Best Health Insurance for Family in India, prioritize the “amount of coverages”. Also, consider the “special benefits” that the insurers include in their offer. Only the “premium amount” should not be your deciding factors.

The experience of being at a hospital billing counter can be incredibly stressful. Simultaneously, a patient’s loved one waits in the discharge lounge. The term “cashless” historically implied protracted paperwork. However, in 2026, the IRDAI New Rules implemented measures to eliminate “Discharge Delay.”

According to the latest IRDAI Master Circular, the power has shifted back to you, the policyholder. Here is how the 2026 cashless process works for your family:

Upon arrival at the hospital, the authorisation process commences. IRDAI regulations now require insurers to decide on the pre-authorisation request within “1 hour ” after receiving it from the hospital.

You no longer need to keep calling your agent from the emergency room. The system is now built to ensure treatment starts almost immediately.

This is the most critical update for 2026. Once the hospital sends the final bill for discharge, the insurer has a strict 3-hour window to grant final authorisation.

In the unfortunate event of a policyholder’s demise, IRDAI requires insurers to process the claim immediately. This ensures the mortal remains are released without any financial dispute.

This rule prevents families from being held “hostage” by hospital bills during difficult times.

IRDAI’s vision for 2026 is 100% Cashless. Even if you are at a non-network hospital, many insurers now offer “Cashless Anywhere.”

ArthikDisha Pro-Tip: It is your duty to intimate your insurer at least 48 hours before a planned surgery. This allows for a smooth hospital entry and exit, similar to a hotel check-out, by setting up the 1-hour approval process in advance.

This Health Insurance Guide 2026 shows that India’s 14% medical inflation needs more than basic insurance. It requires a strategic, proactive approach to claim security. Understanding the 2026 IRDAI regulations, especially the 3-year rule and 5-year moratorium, protects families from claim rejections.

When choosing the best health insurance for family in India for 2026, you should take into consideration comparing Tata AIG and HDFC Ergo. You must assess your city’s healthcare costs and your consumables coverage needs. Review your sum insured and ensure protection under the new regulations immediately, without waiting for an emergency.

Married Women's Property Act India or MWP Act 1874 was enacted in the year 1874…

Official Advisory AY 2027-28 Updates Quick Highlights: Download Form 16 Toolkit ✔ Updated Form 16…

A disciplined 4-step framework to select the best term insurance plan in India, based on…

2026 BUDGET UPDATE Immediate Action: For FY 2026-27, the New Tax Regime is your default…

Download the official ArthikDisha Income Tax Calculator for FY 2026-27. Compare Old vs New regimes…

OFFICIAL ADVISORY 2026 Immediate Action: For 2026, we recommend keeping your annual cash deposits below…

{kind=link}